Elon is right

Rocket man, burning out his fuse up here alone

As this week saw the final collapse into open insults of the Trump-Musk bromance, it’s hard not to just end up laughing. It might feel like one of those Iran-Iraq, Alien v Predator, “a plague on both your houses”, “can’t they both lose?” situations, and to be honest I have a lot of sympathy with that. It’s become a cliche that the right way to understand Trump is through understanding WWE wrestling, and since this whole situation almost doesn’t seem real in a similar way, it’s tempting just to resort to memes.

But what if there’s more to it than that? A specific dispute about the size of the Government deficit led to the social media insults, and it doesn’t seem unreasonable that we should try to take a view on that. And I’m sorry to say that I’m leaning Team Musk on this.

I know that’s not exactly a fashionable view. In academic and progressive circles, expressing sympathy for Elon is probably about as popular as microwaving fish at work. And of course he doesn’t make it easy to like him, whether it’s calling cave rescuers paedos or endorsing the AfD. But equally, as

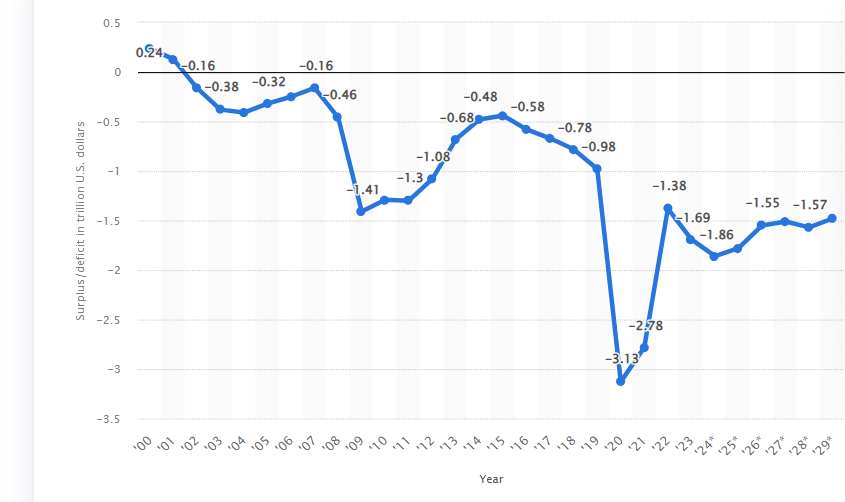

has argued, we shouldn’t let Elon break our brains. So, on the specific point that Musk and Trump fell out about, it might be good to look at some graphs.Here is the US government budget deficit for the last 25 years. It’s not pretty.

Just to be clear on terminology here, this is how much more the government spends than it receives each year. That amount gets added to the national debt, and interest is due on that total. The units are trillions of dollars, so we are talking astronomical sums of money here. Each year, the US debt is projected to go up by about 5% of its GDP.

Of course, there have been two big external shocks on the graph, the 2008 financial crisis and the 2020-1 COVID spending. But it’s striking how little the graph is projected to be returning towards zero, even a decade after the pandemic, and this comes with consequences.

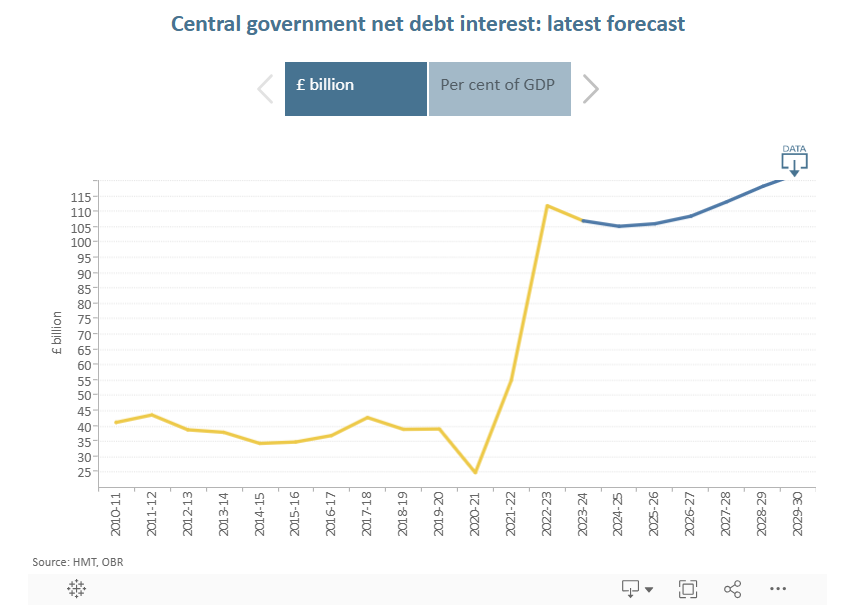

Once again, I’m afraid I am forced to talk about exponential growth. The problem is, once you start adding to the debt, the amount of interest that you have to pay goes up. And the real problem for many western Governments has been that the splurge in COVID spending was accompanied by a jump in interest rates, seriously increasing the total cost of borrowing. We can see the effect of that in the UK:

The cost of servicing our debt more or less trebled overnight, going from £35-40bn a year in interest payments to a situation where “in 2024-25 we expect debt interest spending to total £104.9 billion. That would represent 8.2 per cent of total public spending and is equivalent to over 3.7 per cent of national income”.

I know economists will tell me off for this and point out that countries aren’t like credit cards. But it doesn’t seem very sustainable to me to have a situation where we are borrowing to pay the interest on our debts. Without getting all Mr Micawber about it, there’s a danger of a doom spiral. The more you borrow, the higher the debt becomes, the less reliable a borrower you seem, the higher your interest rates go.

So in this context, I can entirely understand Musk’s concerns about the “Big Beautiful Bill”. Rather than working to push the blue line towards zero, projections that it will add an extra $2.4 trillion onto the debt are, as Musk would say, concerning.

Of course, the problem is that efforts to reduce the deficit, including Musk’s own, haven’t exactly been serious. By focusing on the optics of cruel cuts like “feeding USAID into the woodchipper” and exaggerating their effect to appeal to people like Catturd on Twitter, they have avoided having the tougher conversations about what we can afford these days. And that’s ironic, because the reason that it was at all plausible to put Musk in charge of DOGE is that he does have a track record in this area and might show us the right way to think about things.

There’s a lot of focus on NATO defence spending at the moment. Should it be 2.5% of GDP? 3.5%? Even 5%? But I think that is asking the wrong question. It’s the classic problem of focusing on things that are measurable, rather than things that are useful. I think defence is a perfect example of where spending a few million dollars correctly can be more effective than spending a few billion dollars ineffectively, amply demonstrated by Ukraine inflicting billions of dollars worth of damage on the Russian air force using 117 drones which cost a few hundred dollars each. You could easily increase defence spending in all kinds of ways which would have little effect on your combat effectiveness.

So in my view the question shouldn’t be “what level should defence spending be”, but “how do we develop a culture where we can do stuff like Ukraine?”. We may well need to spend billions of pounds more on expensive bits of metal as well. But in the spirit of focusing on the cuts, I think we should be forensically examining all the systems and working out where targetted increases in spending can have the most effect.

And I’m sorry to say this, but Musk might give us the blueprint for this, and how to “simplify, then add lightness”. By thinking about every part of the launch process, SpaceX have developed a system where “Falcon 9’s price per pound to orbit is roughly $2,700, while NASA’s SLS is a whopping $70,000”. Last year, Space X successfully launched 133 rockets into space, while the rest of the world put together (including NASA, with its $25 billion budget) managed 118. Doesn’t it feel like it might be worth finding out how they did that, and seeing if it is relevant for us?

This isn’t meant to be an argument about public vs private spending, and which is more efficient. But in a world where western countries are facing spiralling debts and demographic challenges, it’s really a call to start thinking outside the box, to be agile, and to try to spend the money right.

In other news, I thought the new Mission Impossible and Clarkson’s Farm were both fine, but not exactly pushing the envelope of their franchises. And for all that people are getting excited about it, I’m not very convinced by the wave-causing potential of the NB.1.8.1 COVID variant (XFG possibly more so, though small sample sizes still). And really when people talk about a wave, I think it’s incumbent on them to say what they mean by that. I don’t think anyone believes we are looking at serious numbers of hospitalizations or deaths - just look at last summer’s “big wave” on the COVID plot on the ONS death dashboard, and tell me how much bigger you think it’s going to be bigger than that.

Being a sufferer of long covid I think that it's not only the death dashboard that needs to be taken into account with covid/viral waves, but the multi year on going costs of people being incapacitated by them. If each infection gives a small but non zero chance of incapacity that lasts years, maybe decades, that could lead to a greater cost to a country than just the emotional cost of people dying.

Another factor in the mix is ‘asset value’. This is often hard to quantify hence not often considered … but is damn key as well. If the additional spend (and debt) is being spent wisely (eg on infrastructure that has a good economic payback longer term) then the additional debt is not a problem, just the same way a mortgage works. However if the additional debt is being spent on day-to-day stuff that has little return … then you’re storing up problems for the future.